Lakeland Property Damage Insurance Lawyer

It is settled law in Florida and throughout the US that insurance companies are bound by a number of duties in dealing with policyholders. Many are contained within the contract for coverage, but one of the most important obligations for insurers is good faith and fair dealing with respect to insureds. This requirement does not sound complicated on its face, but there are challenges with insurance property damage claims. Insurance companies who violate the law or fail to follow the terms of their own policies can and should be held accountable to the policyholders they have wronged by unfairly denying or devaluing their claims.

The Ruel Law Firm specifically focuses on representing policyholders in property damage claims, including commercial and residential property damage. We will advise you and assist you in submitting your claim properly and dealing with insurance company pushback, such as requests for additional information, examinations under oath, delays and denials. We are also skilled at litigation and taking disputes to trial. Please contact us to schedule a consultation with a Lakeland property damage insurance lawyer today. You can also read on for some information on our legal services.

Common Property Damage Claims in Florida

Our office represents property damage insurance policyholders in managing homeowners and commercial claims. We can guide you on claims related to:

- Commercial Property Business Interruption Claims

- Examination Under Oath

- Fire Damage Insurance

- Hail Storm Damage Insurance

- HOA/Condo Association Claims

- Insurance Bad Faith

- Lightning Damage Insurance

- Sinkhole Damage Insurance

- Tornado Damage Insurance

- Water Damage Insurance

- Wind Damage Insurance

Legal Help With Lakeland Property Damage Claims

Regardless of the specific type of claim, our legal services at the Ruel Law Firm will focus on getting your claim paid in full and as promptly as possible. You can rely on an attorney for help with:

- Insurance Coverage Disputes: We will offer recommendations on complex matters related to policy interpretation and application of exclusions. The process requires careful scrutiny of contractual language, as well as evaluation under insurance laws and regulations.

- Examinations Under Oath (EUO): One of the most common tactics used by insurance companies is the EUO, since putting the interviewee under oath is intimidating and gives the insurer ammunition to deny or underpay a claim.

- Bad Faith: If faced with unreasonable delays, improper motives, unsupported denials and other bad faith tactics, we will aggressively pursue claims in mediation, litigation, and at trial for the full amount of recoverable damages.

Steps for Filing a Property Damage Insurance Claim in Central Florida

What’s the proper way to submit a claim for property damage with your insurance company, and does it matter? Is there only one “right” way to present your claim? The fact is that insurance companies will look for any grounds they can find to deny a claim or to limit how much they’ll have to pay out on a valid claim. One of the reasons they often give to deny a claim is to say that it wasn’t filed properly. So, yes, the way you submit your claim is important to get your claim accepted promptly and fully. Below we outline some of the basic steps to filing a claim. If your claim has been denied or you are experiencing pushback from the insurance company and don’t know what to do, the Ruel Law Firm can help. Our attorney Michael Ruel practiced for 15 years in the insurance defense industry and knows how insurance claims work inside and out. Our firm is here to help when your claim is being unreasonably delayed, underpaid or wrongfully denied. Contact our experienced Lakeland property damage insurance lawyer today.

Your first recourse should be to your insurance policy itself and following any procedures outlined in the policy or accompanying information, including using any claim forms provided. You can also call your insurance agent if you are unsure about the proper way to submit a claim. Below are some general steps you should take alongside submitting the claim to the insurance company.

Call the Police

If your property damage is due to a criminal act such as vandalism, arson, or burglary, your first call should be to the police. Keep a copy of any report they make or the case number they give you, as you will likely need to share this information with the insurance company. This step is unnecessary if your claim is based on storm damage.

Notify the Insurer

Although you might have months or as much as a year to submit a claim under the terms of your policy, it is important to notify the insurer about the loss that occurred as soon as possible. Your policy might require you to promptly notify them of any potential claim, and it might include a specific time frame to provide the notice. In some policies, this timeframe is as short as three days after the damaging event.

Submit Proof of Loss

Proof of loss is a statement submitted by you that states the loss you incurred. Your policy might require this proof of loss to be submitted in a particular format, including being signed in the presence of a notary. The proof of loss statement is typically also accompanied by other documentation that proves the loss, such as photos of the damage or repair estimates. Failing to submit a timely and complete proof of loss is a common reason for initial claim denials by the insurance company. Review your policy, call your agent, or contact an attorney to make sure your proof of loss statement is submitted correctly.

Conduct an Inventory of the Property Damage

If items were lost, stolen, or damaged, do your best to create an itemized list. Include whatever supporting documents you have, such as photographs, receipts, appraisals, or values based on comparative shopping. This inventory will be useful when making a claim for the full amount of your damages. Creating the inventory might be an ongoing process as you recall or discover missing or damaged items while sifting through wreckage or by discussing with family and friends.

Mitigate Your Loss

After an area of your home or business has been damaged in a storm, you might need to take some steps to prevent further damage from occurring, such as tarping an exposed hole in the roof or shoring up an unstable area. The insurance company won’t want to pay for any further damage they deem was avoidable, although this can be a point of argument between the company and your attorney whether additional damage was your responsibility or not. While temporary repairs might be necessary to mitigate damages, you typically shouldn’t make any permanent repairs or replacements while your claim is pending. Your attorney can advise you on specifics.

Comply With Insurance Company Requests

The insurer will likely want to come out and inspect the property and assess the damage themselves, and you should provide them with access to reasonable requests. They might also ask for documentation from you, including providing written statements or submitting to an Examination Under Oath (EUO). Call your lawyer if you are unsure about any requests or how to deal with an EUO; you should definitely keep your attorney apprised of any insurance company requests, even if you don’t have questions or feel you need help at this stage. Complying with insurance company requests is a required part of the claim process, provided they are being reasonable with what they are requiring.

Keep the Insurance Company in the Loop

If anything changes regarding the condition of the property while the claims process is underway, you’ll need to let the insurance company know. Always apprise your attorney of any communications you have or plan to have with the insurance company.

Property Damage Insurance Claims Denial

After a storm has damaged your home or business, you might feel devastated by the loss, but at least you know you have property insurance to help you rebuild and recover. That insurance is absolutely critical, and experiencing an insurance claim denial at this point could make you want to sink into despair. Below we take a look at some of the most common reasons insurance companies reject property damage claims and how we can help. An initial insurance claim denial should never be the last word on the subject. You owe it to yourself to get a free consultation from an insurance attorney who can analyze your situation and explore your options with you. For help with storm damage or other property damage claims in Central Florida, contact our experienced Lakeland property damage insurance claim denial lawyer today.

Giving Prompt Notice and Proof of Loss

The longer you wait to file a claim with the insurance company, the weaker your claim becomes. The insurance company could claim that some of the damage occurred after the fact because you let the property sit too long without getting it repaired or that you failed to mitigate your losses as required. Even worse, if your claim is considered untimely, this could give the insurance company grounds to deny your claim altogether. Your policy likely includes a time frame for you to file your claim, and if you wait too long, they can deny the claim under the terms of the policy. The policy likely also requires that you provide adequate documentation that proves the loss. Timely notice and adequate proof of loss are standard provisions in a property insurance contract. An insurance claims attorney can help you put together the proper documentation and advise you on the steps you need to follow. If the insurance company is being unreasonably strict or requiring more documentation than they need just to delay the claim, give them grounds to deny, or hope you give up, then your attorney will hold them accountable and make sure they follow their own rules and the law.

The Damage Is Excluded Under the Policy

A common refrain from the insurance company when you make a claim for property damage is that the specific type of loss you are claiming just happens to be excluded under your policy. You probably thought you were getting a fairly comprehensive policy when you bought it (or else you wouldn’t have bought it), and it can be maddingly frustrating to be told your claim isn’t covered. As a basic premise, unless the damage is specifically excluded in the policy, then it should be covered. However, your policy likely does include lots of exclusions, and it might not always be clear whether a particular claim falls within a stated exclusion or not. For example, some insurance policy language creates an exclusion while other language creates a limitation of coverage; it can be difficult to tell the two apart, but exclusions and limitations are treated differently with different consequences for your claim. We can determine whether your claim was wrongfully excluded under your policy and take the proper steps to get the insurance company to accept your claim.

The Damage Was Pre-Existing

Property insurance policies only cover damage that occurred after the policy was purchased. That sounds perfectly reasonable, but when you go to make a claim, you might find yourself in a dispute over whether the damage was pre-existing or not. For instance, suppose your roof gets damaged in a storm, so you file a claim. The insurance company sends over a roofing inspector who says the roof was already damaged before the storm. How do you prove otherwise? An insurance denial attorney can help prove your claim and ensure that you get paid the appropriate amount for your claim.

The Damage Occurred Due to Wear & Tear

If a pipe suddenly bursts or a roof starts leaking after a hail storm, it’s obvious to you that the damage was caused by a sudden event. The insurance company, on the other hand, might claim that years of neglectful household maintenance on your part (or the prior owner’s part) created the condition that caused the leak. What duty, if any, do you have under Florida law and the terms of your policy to know about the condition of your roof or the pipes in your walls before a damaging event occurs? The Ruel Law Firm takes on complex factual and legal issues like these and helps the insurance company see where they are wrong.

The Application for Insurance Was Inaccurate or Incomplete

At the time you apply for property insurance, you’ll be asked to describe the condition of the property and disclose any defects. When you make a claim for property damage, insurance company inspectors will look closely at the damage. They might allege the roof was already leaking when you bought the policy or there was visible water damage you knew about but didn’t disclose. In that case, they’ll rescind your policy and refund your premiums, but they won’t pay your claim. If the insurance company cancels your policy just to avoid paying a claim, that’s bad faith. Our experienced insurance claim denial attorney will argue the facts in a good faith coverage dispute or hold the insurer accountable for a bad faith rescission.

Property Damage Insurance Claims FAQs

Thousands of property damage claims are filed every year in Florida, and many of them are right here in Lakeland. Even though many people carry insurance that covers this damage, they do not think about making a claim until it becomes absolutely necessary. If your property has been damaged and you need to file a claim, you likely have many questions. Below, our property damage insurance lawyer outlines the most frequently asked questions about these claims, and the answers to them.

What Constitutes Property Damage?

Property damage refers to tangible or physical items, such as damage to a home, personal contents like clothing and electronics, buildings, products.

What is the Process of Filing a Property Damage Insurance Claim?

The first step when filing a property damage insurance claim is to contact your insurer and inform them of exactly what happened. You should also provide them with basic information such as the extent of the damage, the location of the damaged property, and the names of any witnesses who can support your claims. Your insurance company will then provide you with forms to fill out and submit to them. Before you even speak to your insurance company, you should speak to a Lakeland property damage insurance claims lawyer who can speak to them on your behalf and protect your case.

How Should I Respond to a Lowball Offer?

Insurance companies are in the business so they can make a profit. The more they pay out on claims, the less profit they reap. To protect their bottom line, it is not unheard of for insurance companies to deny valid claims. This is one reason it is so important to work with an attorney. A lawyer will negotiate on your behalf and will make a reasonable counteroffer so you receive the full coverage you deserve. Insurance companies are also less likely to try deceptive tactics when they are working with a lawyer and not the policyholder.

What Does Bad Faith Mean?

There are times when an insurance company may legitimately deny a claim. Unfortunately, a lot of the time, insurance companies refuse to make a fair offer or provide the fair coverage policyholders need. In these instances, they may be acting in bad faith. When an insurance company acts in bad faith, policyholders can file a lawsuit against them to hold them accountable for paying fair coverage.

Do I Need to Work with a Property Damage Insurance Claims Lawyer in Lakeland?

You are never required to work with an attorney when filing a claim, but it is highly recommended that you do. At Ruel Law Firm, our Lakeland property damage insurance claims lawyer has extensive experience dealing with insurance companies and will give you the best chance of receiving the coverage you need. Call us today or connect with us online to schedule a consultation with our seasoned attorney and to get more answers to your questions.

Contact Our Lakeland Property Insurance Lawyer to Learn More

Homeowners and business owners in Florida can use a skilled legal partner for pursuing claims for commercial and residential property damage, and the Ruel Law Firm is dedicated to delivering essential support. With well over a decade of insurance defense experience, Michael Ruel is intimately familiar with all the reasons insurance companies give to deny a claim. He knows the law and what facts are important to bring to light when negotiating a resolution or litigating the matter in court. Contact us today to set up a consultation with an experienced Lakeland property damage insurance claims attorney.

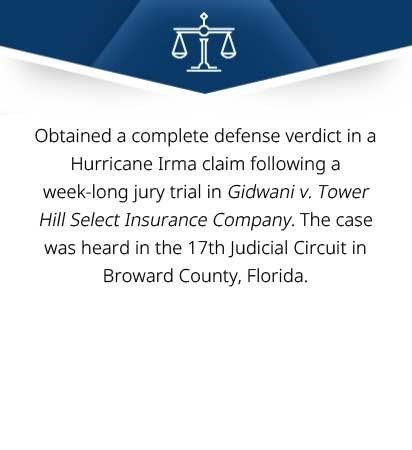

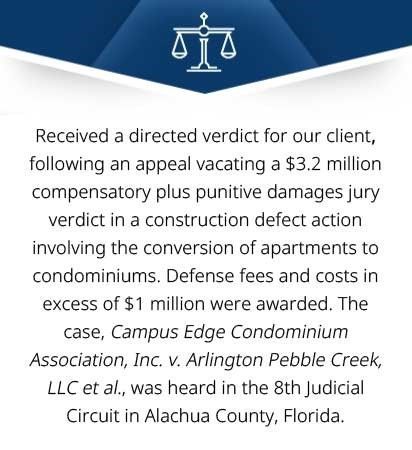

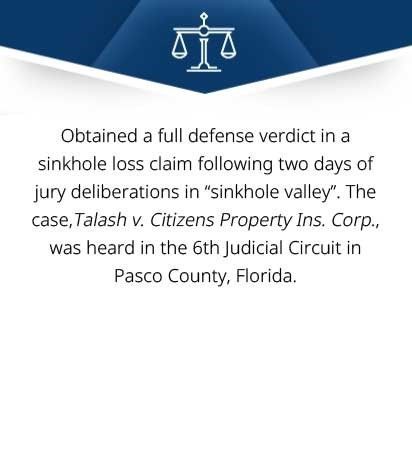

Recent Results

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton